The AFGC State of the Industry 2014 report which is the sixth in series consists of extensive set of historical and updated data which collectively describe the food and beverage, grocery manufacturing and fresh produce sector.

AFGC Chairman Terry O’Brien shared in his Foreword the following key take homes from the report:

"In the food and grocery sector the juxtaposition of growth and declining employment reflects the reality of companies automating to reduce labour cost and drive higher efficiency and productivity.

Notwithstanding the decline, the sector still directly employs just under 300,000 Australians, almost half of those in rural and regional areas. It is vital to the nation’s health and economic wellbeing.

The historically and persistently high Australian dollar is biting, but so too are high input costs, retail concentration and highly restrictive, complex and overlapping regulatory structures. In response, our sector is undergoing a painful adjustment – rationalisation of capacity, closure of smaller plants, and the drive for efficiency and scale.

This report also shows solid export growth in processed food and beverages and a rising trade surplus in food. This trend is a welcome sign that the focus on market access and food export opportunities is paying off.

Of concern is the flatlining of capital investment, at a time when we need an infusion of capital. Food and grocery processing relies heavily on patient capital investment and when there is a reluctance to re-invest regularly to keep pace with technology and its associated productivity improvements, a vicious circle occurs where re-investment lags and returns inch lower over time, and so, capital is even less likely to be attracted.

We need a step change in investment, which requires consideration of carefully focused investment allowances or incentives within the tax system for a period that will provide an ongoing boost to activity, exports and jobs."

The big picture of the industry was broken across the report in chapters highlighting Turnover, Employment, Trade and Capital expenditure and R&D.

TURNOVER

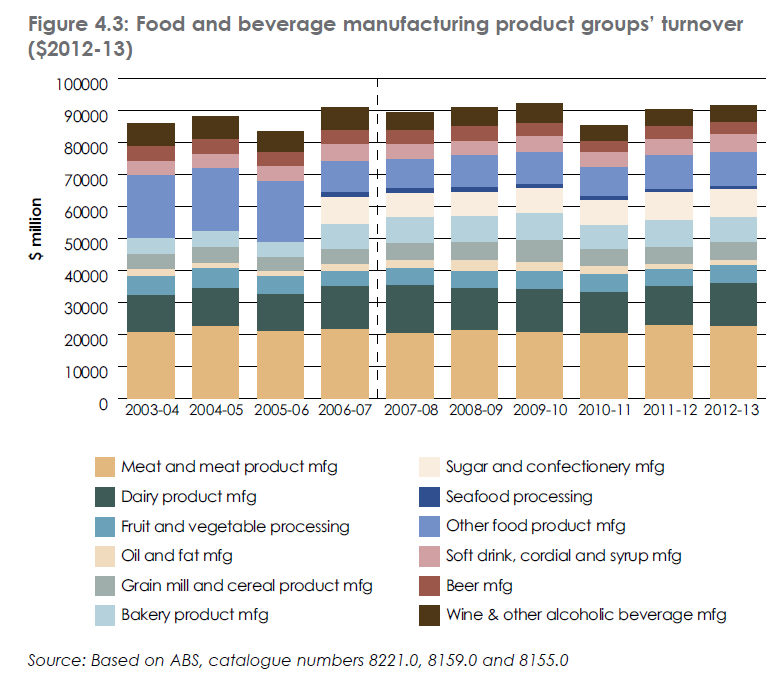

In 2012-13, the food and beverage, grocery manufacturing and the fresh produce industry had a total turnover of $114 billion; food and beverage processing contributed $91.6 billion, grocery manufacturing contributed $16.2 billion and fresh produce $6.2 billion. The industry represents 28.9 per cent of the total Australian manufacturing industry turnover.

Key fact: Meat and meat product manufacturing continues to comprise the largest share (24.6 per cent) of the total sector turnover, contracting slightly by 0.7 per cent in 2012-13. Dairy product manufacturing was the second largest at 14.7 per cent, increasing 9.1 per cent.

Seafood processing comprises the smallest share (1.2 per cent) with a decline of 4.2 per cent in 2012-13.

EMPLOYMENT

In 2012-13, the food, beverage and grocery manufacturing industry employed 299,731 people, representing about 33.7 percent of all manufacturing industry jobs. Total employment consisted of 220,500 people employed in food and beverage manufacturing; 30,529 employed in grocery manufacturing and 48,936 people employed in the fresh produce sector.

This diverse and sustainable industry is made up of over 27,469 businesses consisting of some of the largest globally significant multinational companies to small and medium enterprises.

Key fact: The food and beverage, grocery and fresh produce industry employed more people than the mining and transport equipment manufacturing industries combined.

TRADE

The food and beverage, grocery manufacturing and fresh produce industry accounts for over $55.9 billion of the nation’s international trade. Australia’s trade deficit in this industry is $1.8 billion, with total imports in 2013-14 valued at $28.8 billion and exports valued at $27 billion.

Key fact: Meat processing exports continue to dominate Australia’s food and beverage exports at $10.5 billion, an increase of 24.5 per cent over the previous year.

CAPITAL EXPENDITURE and R&D

The Industry spent $541.8 million on research and development (an increase from the $513.9 million in 2010-11) and $3.1 billion on capital investments to improve business productivity.

Key fact: The sub-sector with the largest expenditure on R&D was the dairy product manufacturing sector ($109.3 million), followed by meat and meat product manufacturing with $95.9 million.

Download the full State of the Industry Report 2014